Much Ado About Central Banking

Q: Why are central banks so boring? A: Because they have low interest rates!

Welcome to the Global Capitalist — A free newsletter on international developed, emerging and frontier markets viewed through the lens of history and culture.

Hi everyone — Apologies for the pun at the top. I’m going to try something new next week so bear with me.

This one is long, so feel free to skip around or come back to it later. I think you all will enjoy it!

— Tom

Much Ado About Central Banking

Why are central banks so boring?

Because they have low interest rates!

I’ll see myself out...

Lately, interest rates and central banking have become the topic du jour across global capital markets. Indeed, the collective fiscal reaction to the COVID recession has spurred ceaseless debates about the future of our global economy.

For some, the unprecedented levels of fiscal stimulus and monetary easing paint a bitter picture of our economic future — a future stymied by hyperinflation and currency debasement. In contrast, others have celebrated the emergence of a new policy regime, underscored by the principles of Keynesianism and government intervention. Surely, the outcomes of the CARES Act has shown us that targeted fiscal stimulus can be extremely effective in achieving certain (nominal) policy outcomes — especially compared to the efficacy of monetary policy.

Make no mistake, however: this is an experiment with an indefinite realized outcome. Then again, of course, we’ve learned not to get too comfortable with our conventional economic wisdom.

When considering the implications of monetary policy, it’s imperative to remember that not all policy rates are set equally. We explore below:

Brazil

South America’s largest economy has seen calmer days, to say the least. For starters, the coronavirus appears to be an after-thought for Bolsonaro and his administration, despite a perpetuating climb in daily cases and deaths. President Bolsonaro, who had once boasted the highest approval rating of any world leader last year, has seen his fandom vanish following a series of scandals tied to his administration. Keep in mind — corruption was a key “pain point” during Bolsonaro’s victorious 2018 campaign, as the infamous Lavo Jato animated the Brazilian electorate.

Speaking of Lavo Jato... former President Luiz Inácio Lula da Silva (Better known as “Lula”) was relieved of his corruption charges last month on the basis of a “biased jurist”. Justice Minister Sergio Moro, the jurist who had served Lula’s sentence in 2018, was ominously promoted to Minister of Justice not too long after Bolsonaro’s presidential victory.

As of this writing, Lula is the favorite to win the Brazilian General Election, which is scheduled to take place next year on October 2nd, 2022.

Onto central banking...

The other week, the Banco Central do Brasil (BCB) lifted interest rates (the SELIC rate) for the first time since 2016.

Inflation printed 5.20% in February, prompting the Central Bank’s committee (the Copom) to hike rates by 75bps versus consensus estimates of 50bps.

The current SELIC rate is 2.75%.

Brazil’s Ibovespa is down over 3% year-to-date.

Financial Times: Inflation fears prompt Brazil to lift rates for first time in 6 years

Before the decision, Alberto Ramos, Latin America chief economist at Goldman Sachs, said a normalisation of monetary policy was “in order” in Brazil, but there was “no reason to hit the panic button at this stage”.

“It’s a balancing act between an economy that’s weak and [inflation] headwinds that have intensified in the short-term,” he said. “They can’t really hike too much because the economy is pretty weak.”

—————————

A steeper Selic may also provide some support to the exchange rate, which has weakened as investors worry about government spending and borrowing levels. The Brazilian real is among the worst-performing major emerging market currencies this year.

William Jackson, chief emerging markets economist at Capital Economics, said fiscal concerns “have made foreign investors wary about investing in Brazil”.

“The other is that real interest rates are so low, probably minus 1.5 to minus 2 per cent,” he added.

Russia

Once again, Russian President Vladimir Putin and the Russian Federation have found themselves at the heart of an egregious infraction of democracy and human rights. The attempted assassination (and eventual imprisonment) of Kremlin critic Alexey Navalny has reminded the world of how illiberal Russia’s “democracy” really is.

As anticipated, the Kremlin has deflected all accusations of wrongdoing, even going so far as accusing the long-time Putin critic (who Putin almost exclusively refers to as a “blogger”) of poisoning himself with a Soviet-Era nerve agent. Before his arrest, Navalny had released a 2-hour documentary (shown above) featuring a $1.5 billion palace allegedly owned by President Putin. As of this writing, the video has over 115 million views.

Nevertheless, Putin’s blatant nihilism towards democracy and the rule of law has incensed the Russian populace. In late January, protests broke out across nearly 200 cities to protest Navalny’s imprisonment, resulting in over 1,600 arrests. Curiously, amidst the peak of the protests, large swaths of the country lost access to social networking platforms like YouTube, Twitter, and Google. While Russian authorities have attributed this outage to a datacenter fire, Google has challenged these claims.

Fortunately, the world’s stewards of democracy are familiar with the malice of Putin’s regime. Last month, the European Union invoked the “Magnitsky Act” in issuing sanctions on Russian nationals involved with Navalny’s poisoning. U.S. Secretary of State Antony Blinken would follow suit shortly thereafter, invoking the breadth of the U.S. Chemical and Biological Weapons Control and Warfare Elimination Act of 1991 in levying sanctions on those same Russian officials.

Democracy Reigns: The Magnitsky Act was lobbied by which famous British/American investor? Answer below.

Central Banking? I’m glad you asked!

Last Friday, the Central Bank of Russia (CBR) issued a rate hike of 25bps, the Bank’s first hike since 2018.

Russian CPI grew 5.7% in March, the fastest pace since 2016. Similarly, December real wages grew 4.6% (YoY) vs. forecast estimates of a -1.5% contraction.

The CBR’s decision stems from a rapid acceleration in inflation expectations. The bank’s current inflation target is 4.00%.

The Ruble has depreciated ~3.25% against the dollar and is unchanged versus the Euro since the beginning of the year.

Following the hike, the CBR’s key rate stands at 4.50%, just above all-time lows.

Bloomberg: Russia Surprises With Rate Hike, Signals More to Come

The central bank considered a bigger increase on Friday, but decided that policy changes should be gradual, Governor Elvira Nabiullina, who was wearing a brooch in the shape of a hawk, said at a news briefing after the decision.

“Time is of the essence,” she said. “If you postpone a rate hike, inflation may accelerate and inflation expectations won’t decrease. This will move inflation further from the target and that will require a more significant rate hike in the future.”

The ruble climbed and 10-year bond yields rose to their highest level in a year.

——————

The threat of new U.S. sanctions has clouded the outlook for the ruble, which could add new inflationary pressures in coming months. Relations between Russia and the U.S. reached a new low this week after U.S. President Joe Biden vowed to make the Kremlin “pay a price” for election interference.

Turkey

The Republic of Turkey is notorious for espousing some rather paradoxical monetary philosophies. Specifically, Turkish President Recep Tayyip Erdoğan is a vehement opponent of high interest rates, believing that higher rates, not lower rates, beget inflation. Of course, conventional economic theory (and the struggles of the Turkish Lira) would contend that belief. Yet, Erdogan, who once referred to higher interest rates as “the mother and father of all evil” has squashed any semblance of monetary hawkishness.

The other week, the Central Bank of the Republic of Turkey (CBRT/TCMB) hiked their seven-day repurchase rate by 200bps, reaching a near-world-high of 19.00%. Erdogan was clearly displeased with the Bank’s decision, as he fired Naci Agbal two days following the rate hike. For context, Agbal was Turkey’s third Central Bank governor in the last two years.

Erdogan’s hawkishness persists despite reeling double-digit inflation and economic deterioration. Turkish inflation has averaged 14% per annum and economic output is down roughly 20% from its 2013 highs. Sure, the Turkish economy eked out a nominally positive growth rate in 2020, but at what cost? The Lira has depreciated considerably against developed market currencies like the Dollar and the Euro.

What else? (Central Banking)

The Central Bank of the Republic of Turkey (TCMB) hiked rates by 200bps last Friday. The current 1-week repo rate stands at 19.00%.

Through 3/31/21, the Borsa Istanbul 100 shrank 6%.

Garanti (BIST: GARAN) — Turkey’s largest bank — is down 32% YTD. BBVA, one of South America’s largest banks, owns a 49% stake in Garanti’s business.

Şahap Kavcıoğlu, Turkey’s new Central Bank governor, has committed towards keeping Turkey’s policy rate above the rate of inflation.

Al Jazeera: Turkey’s new central bank boss to hold talks with bankers: Report

In his less than five months in the job, Agbal had increased the key rate to 19 percent from 10.25 percent, including a 200 basis point rise on Thursday to head off inflation near 16 percent and a recent lira slide.

His hawkish stance lifted the lira from record lows beyond 8.5 per dollar in November, dramatically cut Turkey’s CDS risk measures and started to reverse a years-long trend of funds abandoning local assets.

The lira had gained more than 3 percent since Thursday’s rise.

Daily Sabah: Policy rate to remain above inflation, Turkish central bank chief says

"The high levels of inflation and inflation expectations in the current period require a strict monetary policy stance," Central Bank of the Republic of Turkey (CBRT) Governor Şahap Kavcıoğlu told the bank's annual general assembly meeting in the capital Ankara.

"We will continue to use all the tools we have, independently and effectively," Kavcıoğlu said, reiterating the commitment to bring inflation down to 5%.

Everyone’s a Dove

Quite frankly, the aforementioned countries pose an exception to most of the central banking activity occurring across the world. Generally speaking, central bankers have been extremely accommodative with regards to the coronavirus recovery. As of this writing, thirty countries carry a key rate of 0% while another nine countries yield an uninspiring 25bps. Collectively, over 50 of the world’s central banks offer a benchmark yield lower than 1%.

Yet, if we are to take central bankers at their word, rates should remain this way for the foreseeable future.

Real Interest: Can you name three other countries which issued rate hikes so far in 2021? Answer below.

Deflation? In this Economy?

Yes, quizzically enough, deflation still poses a risk for segments of the world economy, despite the largess of fiscal and monetary aid. Granted, much of this peril can be loosely traced to the dismal recovery of the Eurozone Crisis — although that is a topic for another time.

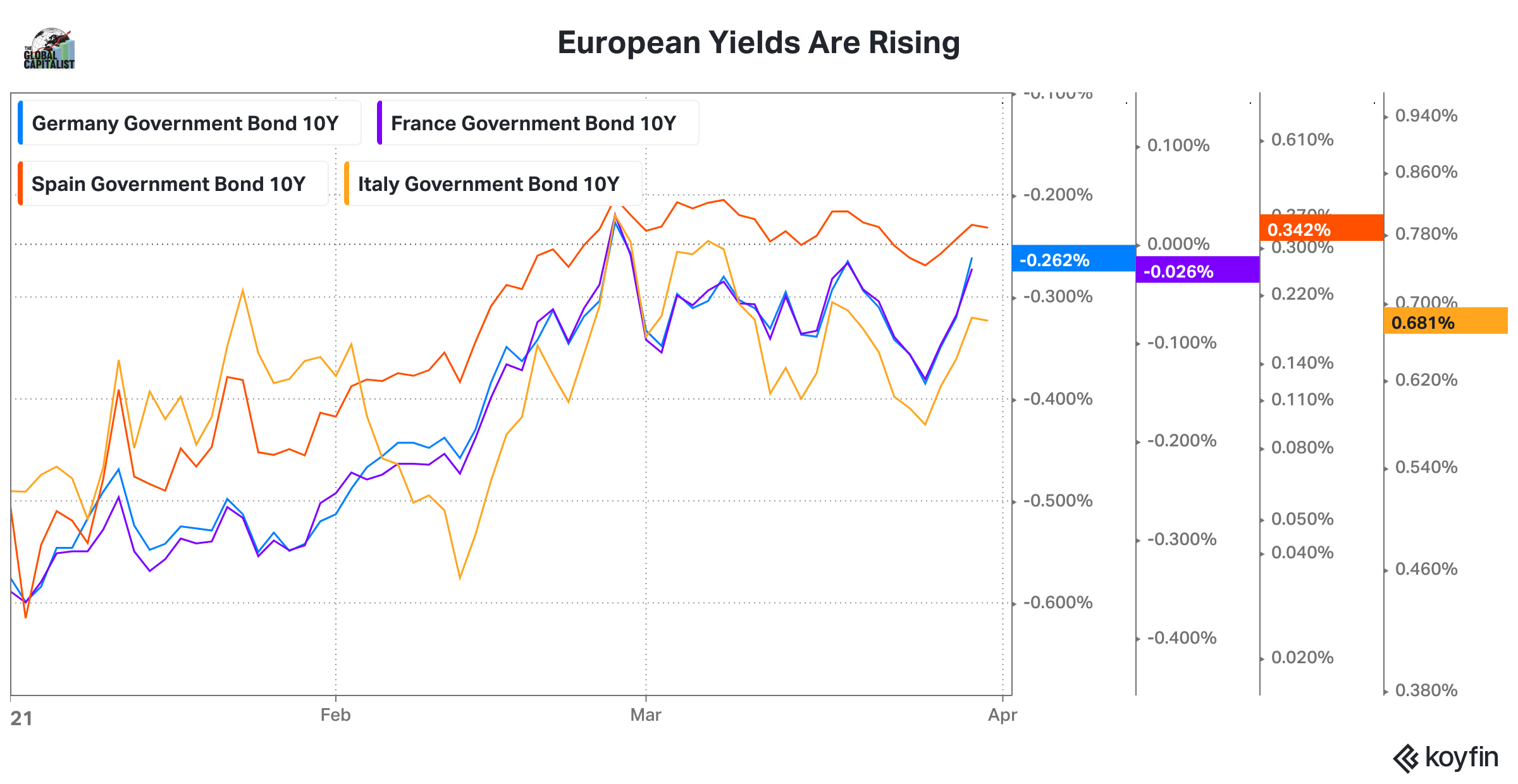

Nevertheless, the Eurozone is still teetering on deflation, as the EU recorded five straight months of price contraction last autumn. While the bloc has shown an improvement in CPI growth this year, ECB President Christine Lagarde remains devoted to the Bank’s asset purchase program(me), scooping up bonds at a clip of roughly €20 billion per month. This, however, has been futile in compressing European yields. Spain, Greece, Italy, Germany, and France have all seen their 10yr yields soar by over 30bps this year.

Fundamentally, this represents a rise in inflation expectations — generally a good thing for a disinflationary economy like the E.U! However, ECB leadership has been adamant in their desire for lower yields, believing that looser monetary policy would engender stronger real economic growth. Then again, this thesis has yet to play out in their favor.

Also, European rates have been so breathtakingly low for so long that this ongoing “bond selloff” really doesn’t mean all that much1. Indeed, the cardinal risk to the Eurozone’s recovery lies within the inefficacy of their tools. This isn’t to say that the ECB is constrained in their open market operations (there is nominally no limit as to how much debt the Bank could add to its balance sheet). Rather, the question is as to what tools the E.U. could leverage in achieving its goals. Investors, economists, and government officials alike are gradually losing confidence in the potency of quantitative easing as a method of stimulating growth.

Perhaps there is a French translation for “stimmy”?

Market Insider: Christine Lagarde calls rising bond yields 'undesirable' as ECB steps up purchases to soothe the market

European Central Bank chief Christine Lagarde said on Thursday the recent rise in bond yields could have an "undesirable" impact on the economic recovery, after the ECB announced it would ramp up the speed of its asset purchases to try to calm the market.

The Eurozone's central bank left its coronavirus bond-buying envelope at 1.85 trillion euros ($2.21 trillion) and its key interest rate at -0.5%. But it said it would "significantly" step up the pace of its purchases within the asset-buying scheme over the next three months.

Lagarde said in a press conference after the decision that the ECB was responding to a rise in "market interest rates" including bond yields, which have climbed rapidly in recent weeks and weighed on market confidence.

"If sizeable and persistent, increases in these market interest rates, when left unchecked, could translate into a premature tightening of financing conditions for all sectors of the economy," she said.

Of course, the ECB is not alone in their dovish endeavors. The Bank of Japan (the dove-iest of all dovish central banks) has maintained a similar consistency in their easing strategies — again — to little avail. Indeed, Japanese inflation has averaged a mere 0.10% since 2000, considerably lower than the Bank’s long-term target of 2%. In pursuit of this metric, the BoJ has accrued a balance sheet totaling over ¥700 trillion in assets, equivalent to about $6.5 trillion in dollar terms.

Then again — the swelling size of central bank balance sheets doesn’t seem to scare anyone anymore — and why would it? Inflation is all but present in the world’s largest economies, despite continued asset purchases and monetary easing. Thus, it begs several questions: How effective are these programs? Are we wrong about economic theory? If these programs continue to be ineffective, how much longer will they continue? And how will they unwind?

Recently, the BoJ quietly retreated from their ETF purchasing program, relieving themselves of a ¥6 trillion annual commitment towards ETF purchases. Mind you, this does not mean the Bank is completely halting their operations. Instead, the BoJ claims they are rescinding these commitments to ensure greater flexibility in their relief efforts. Historically, the BoJ has forayed into the equity markets when the market falls 50bps during the morning session2. Nevertheless, one might ask if this decision reflects the Bank’s acknowledgement of the inability to stimulate inflation through the equity markets.

What’s more, there is also concern as to how this program will eventually unwind. As of early March, the Bank of Japan is sitting on a $120 billion capital gain, representing roughly 7% of the entire Tokyo Stock Exchange.

MarketWatch: Bank of Japan drops stock-buying target

On Friday, it dropped the ¥6 trillion target but reiterated it was ready to step in with larger purchases if needed. It said the higher purchase limit, previously described as a temporary pandemic response, would continue even after the pandemic subsides.

The move came after a rapid rise in stock prices over the past year that has brought the Nikkei Stock Average near a 30-year high. As of March 1, the BOJ's stockholdings were worth more than $450 billion, according to NLI Research Institute, making it the single largest holder of shares in the Tokyo market.

————————————

The BOJ said the 10-year Japanese government bond yield could move more freely around its zero target. It said it would let the 10-year JGB yield move in a range between minus 0.25% and plus 0.25%. The target range, put in writing for the first time, compared with previous verbal guidance that put the band roughly between minus 0.2% and plus 0.2%.

Indonesia’s economy, in a similar light, has been crippled by their own disinflationary dilemma. Last summer, Indonesian CPI contracted for three consecutive months, driving undesired tailwinds behind the Indonesian Rupiah and signaling Indonesia’s first recession since 1997. What’s more, despite countless reductions in Bank Indonesia’s key rate and the unveiling of a new treasury purchasing program last spring, the nation has yet to meet the central bank’s target of 2—4% inflation. Not to mention, a meager CPI reading in February prompted Bank Indonesia to cut their 7-day repo rate to an all time low of 3.50%.

We’ve spoken previously about the role of foreign exchange in economic development. Disinflation (not to be confused with deflation) is especially perilous for an emerging economy as a country risks pricing themselves out of their economic advantages. In Indonesia’s case, the undesired strength of the Rupiah has obstructed their economic recovery as Indonesian exports grow more expensive on an exchange-adjusted basis. Since April 2020, the Rupiah has appreciated 10% against the Dollar, 12% against the Yen, and 2% against the Renminbi. Concurrently, Indonesian exports fell 6.2% through July of last year as GDP is expected to contract by roughly 2% in 2020.

Finally, tourism — one of Indonesia’s chief economic engines — has effectively vanished, depressing the country’s economic potential and hampering the country’s long—term developmental goals. Foreign visits were down over 80% in February versus the year prior.

Despite the clear messaging from Indonesia’s central bank, investors and economists alike are forecasting at least one rate hike from Bank Indonesia in 2021, as forthcoming inflation will likely persuade the central bank to hike rates earlier than anticipated. Similar to other 10yr treasuries found across the globe, the Indonesian 10yr has soared above 6.75%, from 6.00% in January.

Surely, Bank Indonesia must be working on their own “Dot Plot” to help quell the ongoing bond selloff.

Trivia

Democracy Reigns: Bill Browder, the founder of Hermitage Capital Management, is known as the architect behind the Magnitsky Act. Browder details his journey in getting this act implemented and passed in his memoir Red Notice.

Real Interest:

Georgia (50bps — 8.5%)

Zambia (50bps — 8.5%)

Burundi (60bps — 6.6%)

Ukraine (50bps — 6.5%)

Kyrgyzstan (50bps — 5.5%)

The Global Capitalist

Follow us on Twitter / Instagram

Follow Tom on Twitter

**If you subscribe through Gmail, please move us from your ‘Promotions’ tab into your ‘Primary’ inbox so you never miss a letter!**

**None of this should be taken as investment advice. Do your own research or speak with an advisor before investing in emerging or frontier markets.**

At least for now!

The Japanese Stock Exchange has two sessions — Morning & Afternoon.