A Framework for Business Analysis Through the Lens of Capital Allocation

“In large part, companies obtain the shareholder constituency that they seek and deserve.” - Warren E. Buffett

Hey all —

It’s been a while, so I decided to write a little about capital allocation.

It’s a little long (and perhaps boring to some), so no hard feelings if you don’t read it, I promise.

Happy Summer!

Tom

i) Introduction

The core impetus of a business is to generate an accounting profit. More often than not, this is created by grossing revenues greater than the aggregate cost of doing business1. This is far from a novel concept: The renowned economist, Milton Friedman, was notorious for his assertion that companies should be run to maximize shareholder profit. After all, a company’s shareholders are the beneficial owners of the business and are interested in seeing the value of their ownership increase. The concentration of this constituency helps to align interests and drive consensus among interested parties.

The existence of “shares” is not exclusive to publicly traded companies. Start-ups, housing cooperatives, and private equities are also typically underscored by a joint stock structure, in which fractional ownership is represented by shares of stock. A company’s shareholders, while not directly active in day-to-day operations, can exercise influence onto a business through board representation and voting2. The board, on the other hand, is responsible for hiring management and guiding the company’s strategy towards making profits. Companies tend to compensate both the C-Suite and the board with stock awards, option grants, and other equity-related forms of pay as a means of aligning incentives and eliminating conflicts of interest.

Contrast the dynamics above with the principles of stakeholder capitalism, which suggest that corporations have obligations beyond their shareholders. More succinctly, corporations have an obligation to all stakeholders - encapsulating regulatory bodies, local communities, and anything or anyone else that may be influenced by the existence of the business. This strokes a broad brush across the gamut of economic externalities and appears to be intentionally vague – for reasons we’ll get to later.

While not entirely congruent, stakeholder capitalism is promulgated by the institutional adoption of the environmental, sustainable, and governance (ESG) investment framework. The ESG strategy seeks to favor (invest in) companies that practice sound governance and are mindful of things like carbon footprints, net emissions, and progressive social values. Negative economic externalities, if you will. The crux of this ideology stems from the fact that all companies are somewhat interconnected and should therefore prioritize the benevolence of society over the well being of their shareholders. A proponent of the ESG framework might argue that oil drillers should stop drilling because a warming climate will drive up the cost of food production. An increase in food costs would precede lower discretionary incomes, which would mean fewer people buying iPhones – so on, and so forth.

Another read of the ESG mandate might suggest that shareholders, both institutional and retail, own many stocks or broad-market index funds. As a fiduciary, it is your obligation to maximize the aggregate value of their shareholders portfolio rather than the value of an ESG unfriendly company. In addition, stocks generally move in the same direction (beta, for the uninitiated3). By maximizing societal benefits, a roaring bull market could help boost the shares of an ESG unfriendly business. Then again, shareholder value can be maximized in other ways besides boosting profit margins, but again we’ll come back to that later.

Let’s assume there’s an extreme third school of thought which argues that corporate profitability is inherently exploitative because a company's employees (laborers) are entitled to the total value of their production. In this vein, an accounting profit implies that someone else (a capitalist, usually) is reaping the benefits of (exploiting) someone else’s work. While popular among certain niche political systems, the reality of today’s labor market consists of collective, symbiotic relationships between employee and employer. Furthermore, publicly-traded and other joint stock enterprises can compensate non-shareholding employees with benefits including stock options, 401(K) matching and other forms of capital as a means of attracting talent and aligning interests.

To summarize thus far – companies seek to make profits to benefit their shareholders. Shareholders can be composed of a variety of parties and are generally interested in maximizing the value of their shares.

Yet, in spite of this supposed gold standard of capital allocation, a simple screen run at the end of Q2 ‘23 reveals over 300 publicly traded companies with positive share-based compensation (often to the tune of hundreds of millions of dollars), negative earnings (net income), and net cash outflows. What gives?

A scrutinizing read of this dynamic might accuse the enterprise of being run solely for their workforce at the expense of shareholders. Outside shareholders would presumably be upset over the absence of profitability and the cost of dilution from share issuance. On the other hand, any form of worker compensation, including share-based compensation, is an operating expense. Many businesses, particularly service-oriented businesses, are only as strong as their workforce, or human capital will allow them to be. Losing human capital and the relationships that tag along can be fatal in the corporate world. Companies that rely upon the prowess of their human capital are prudent to reduce employee turnover and departures to rival firms.

Again - there are technicalities! There are companies who are unprofitable, although yield positive cash flows through non-cash equity compensation, working capital drawdowns, and other balance sheet mechanisms. Assuming there are no outside shareholders, companies with these characteristics appear to be the closest thing to model #3 – reserving company profitability exclusively for the company’s employees, regardless of shareholder overlap.

ii) The Etymology of Capital

The model of a business is rather simple. Financiers provide an enterprise with capital, typically in the form of debt (loans) or equity (ownership). The company uses that capital to figure out how to make more money and generate an accounting profit. Once a company is profitable there is theoretically no need for additional capital4. Companies stuck with too much capital are known to be “overcapitalized” and will often seek to return excess capital back to shareholders.

Once a company is profitable, the company’s financiers will look to get their capital back (and then some) in exchange for the risk incurred. In the case of debt, creditors’ primary concern is conservation of capital. Lenders will structure their loans against something safe like the company’s tangible assets or income streams. The creditor can sleep soundly at night knowing there is recourse in case the loan isn’t paid back.

Equity, on the other hand, is innately more riskier. Unlike debt, equity simply represents ownership in the company and a junior claim on assets. In the case of insolvency, senior debt holders must be made whole before equity holders get anything. In exchange for this risk, equity returns are undefined and potentially infinite. Equity is appealing to investors because of this risk profile and, unlike debt, does not have a defined “payback period” in which capital must be returned.

Tapping the equity markets, however, comes at a cost: Issuing or selling new shares dilutes existing shareholders’ ownership in the business. Unprofitable businesses, as an example, might prefer to issue equity to reinforce working capital and sustain operations given that they do not throw off enough cash to cover interest expenses. Not that they have much of a choice! Again – lenders are interested in preservation of capital over financial return. They likely wouldn’t be interested in lending to an unprofitable company.

The function of returning capital to equity holders is a little trickier than debt. As highlighted earlier, debtholders are enshrined with seniority in the cap structure and are paid periodic interest before receiving their principal investment. Equity holders, by contrast, see capital returned in the form of dividends, buybacks, or a sale of the business – although none of these outcomes are guaranteed, even if the company nets a profit. This limited tool set of returning capital to shareholders is one of several reasons why a public listing is so monumental: The ability for investors to liquidate shares on a public exchange enables earlier financiers to secure a return on their capital without diluting other shareholders or drawing down company assets.

What about remaining shareholders? Well, that would take us back to our core theme: Company management is tasked with maximizing shareholder value, usually by growing earnings and cash flows5. Companies will leverage the liquidity provided by the capital markets to reach profitability, as one does when seeking to optimize shareholder value. Floating shares of a company on a public exchange enables investors to obtain a return on their capital without influencing existing shareholders. A public listing serves to reduce the company’s cost of capital while providing liquidity to shareholders and financiers.

iii) The Triangle

It is said that corporations receive the shareholders they deserve. In other words, management teams attract investors based upon how they allocate capital. A retiree, for instance, might have a larger allocation to dividend-paying stocks compared to a younger investor. The issuance of a dividend instead of, say, a new R&D initiative, being a significant capital allocation decision.

On the other hand, a company that is promising new products many years out into the future might have their shareholder demography composed of speculators and momentum traders, opposed to conventional buy-and-hold funds and investors. This dynamic is accentuated by institutional investment mandates – dividend funds own dividend paying stocks, tech funds own tech stocks – so on, and so forth. Infamously, Exxon Mobil suspended their company’s 401(K) match in the summer of 2020 so they could maintain their dividend and keep their stature within “Dividend Aristocrat” funds.

Again, this is a significant capital allocation decision! The removal of Exxon from dividend aristocracy would’ve torpedoed the company’s stock price as managers moved to dump their shares6.

Indeed, capital allocators and management teams are confronted by a plethora of constraints in the pursuit of maximizing shareholder value. Not to mention, companies today need to adhere to the seemingly infinite needs of stakeholders, spanning far beyond shareholders and employees. The opportunity costs that emerge in appeasing all stakeholders (equity holders included) presents an intuitive framework for understanding businesses and their capital allocation strategies.

Below, I depict what I call “the Triangle of Capital Allocation”, depicting the trade-offs evident in the pursuit of maximizing shareholder value. The idea reads that the constraints of capital allocation are narrow – companies can optimize for, at most, two of the three constituencies:

Shareholders

Customers

Employees

Optimizing for two-of-three constituencies doesn’t necessarily mean ill intent towards the missing third. The reality is that there are inevitable concessions that must be made in how and where a company spends its money. A price hike, as an example, might be beneficial for shareholders & employees (wider margins, reduced sales quotas) but detrimental to customers. Companies seeing turbocharged top-line growth may look to appease customers (lower prices) and employees (compensation incentives) without a blueprint of how to return capital to shareholders.

iv) Companies Run for Investors:

Companies that are run for shareholders are generally characterized by their emphasis on shareholder value. These companies, if public, tend to be supported by proactive investor relations teams tasked with conveying the company’s strategy and benchmarks for capital returns. As discussed before, there are three main ways of returning capital to equity holders: Share buybacks, dividends, or a full sale of the business.

A full sale of the business is the simplest and most straightforward method of returning capital – a buyer simply buys all of the outstanding shares of the company for cash or equity considerations7. The buyer typically bids a premium to fair market value as any acquisition is subject to investor approval. Cash received upon the closing of an acquisition can be spent or allocated elsewhere.

Share buybacks serve a different (albeit similar) function in the capital returns equation. In lieu of a full sale, companies will often undertake share buyback schemes to try and maximize shareholder returns. Fundamentally, a company buying back their shares must purchase their shares from (provide cash to) existing investors. Assuming those shares remain in the company’s treasury, existing shareholders benefit from a step-up in ownership and a greater claim on the company’s cash flows. Once again, cash received from buybacks can be spent or reallocated into other securities.

Finally, dividend issuance appears to be the most linear path of returning capital to equity holders as a dividend is merely cash paid out from the company’s earnings. The bond-like elements of a dividend appeal to investors looking for stable income streams as there is the perception of safety and predictability. Companies that maintain and hike their dividends over time are known as dividend aristocrats and can benefit from capital flows into dividend growth funds.

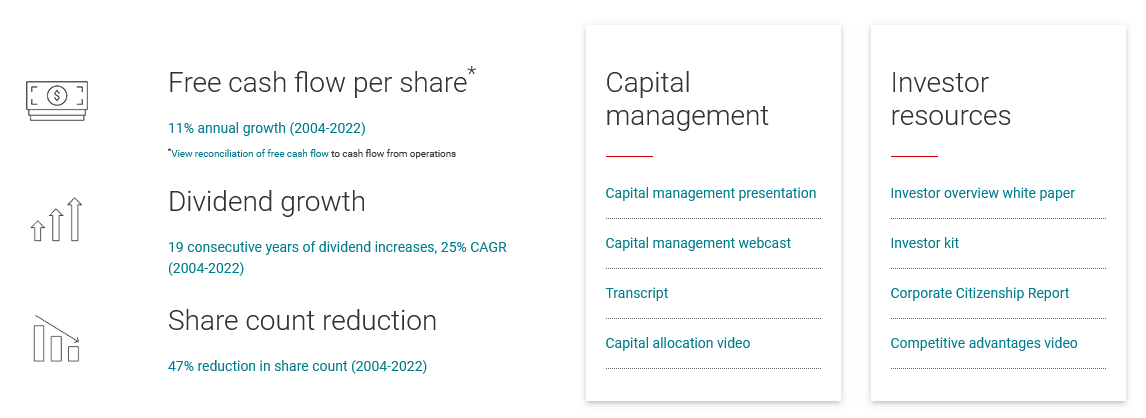

Texas Instruments (NYSE: TXN), featured in the screenshot below, exemplifies a business that prioritizes shareholder value. The company begins their Investor Relations page by highlighting three KPIs specifically geared towards shareholder value creation. The hyperlinks in the two rightmost columns serve to supplement investors’ understanding of the left-hand side with videos (“Capital Allocation”), papers (“Investor Kit”), and other resources.

Note that the luxury of being a “shareholder-run” enterprise can be elusive for many enterprises. Surely, every company would like the luxury of sharing positive, shareholder-friendly results on a quarterly basis. Again, the constraints of capital allocation help to reveal the primary focus of any enterprise.

v) Characteristics of Customer-Focused Businesses:

“We’re not competitor obsessed, we’re customer obsessed. We start with what the customer needs and we work backwards.” — Jeff Bezos (former CEO, Amazon)

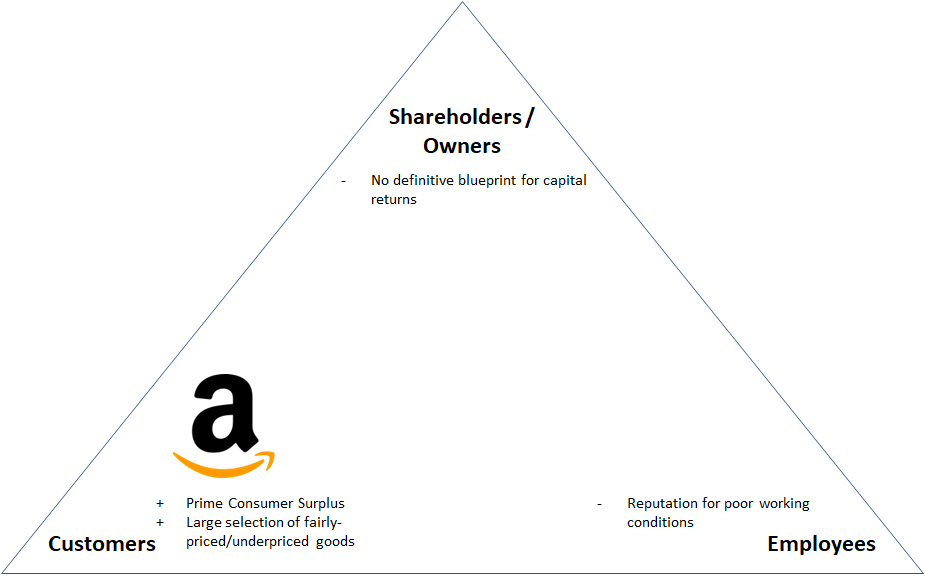

One of the many virtues of capitalism is that it is an inherently democratic system. With the exception of local monopolies and regulated markets – consumers pay for goods and services from the companies they wish. Businesses have built incredible brands upon an ethos of customer obsession, successfully differentiating their offering in what is, in many cases, a commoditized market. Amazon stands out in this instance - the Prime membership is often credited with generating a consumer surplus for Amazon’s customers. Users on the platform are, in essence, receiving more value than what they’re paying for from perks like free shipping, streaming, and more.

Perhaps uncoincidentally – Amazon was unprofitable until 2015, going nearly two decades as a public company before generating an accounting profit. Again – this can be seen as a technicality: The absence of profitability was offset by positive cash flow generation and explosive top-line growth. Amazon’s share of the global retail market spiked as customers grew accustomed to their vast catalog and expedient shipping. Meanwhile, Amazon stock stood out as one of the top performing names of the 2010’s, compounding 33% per annum between ‘10-’20. Shareholders, by virtue of customer obsession, benefited from the company’s aggressive, albeit articulate, go-to market strategy.

Now consider the outstanding party – Amazon’s employees. Without leaning too hard into narratives and headlines, Amazon is perhaps most infamously known for their tough working conditions and relatively meager pay. A simple Google Search for “Amazon Working Conditions” yields over 2B results, most of which do not paint Amazon as a champion of labor. Indeed, while Amazon promotes competitive wages for their 1.5MM employees, critics of the online retailer have accused the company of sub-optimal working conditions and grueling oversight of warehouse workers. It is perhaps revealing that Amazon has fended off several attempts at unionization, despite the lucrative benefits offered to their workforce.

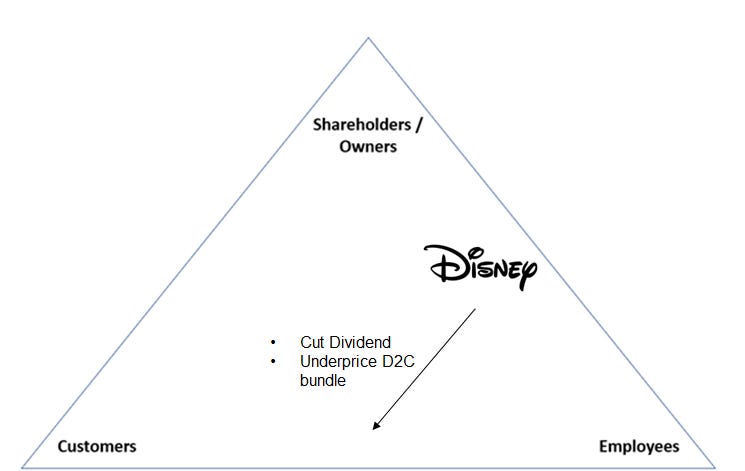

Beyond Amazon, recent events surrounding the entertainment business have shone light on how studios and the owners of intellectual property have eschewed the interests of their talent amidst the industry’s digital transformation. Specifically, the emergence of streaming platforms has upended the cinematic business model – kneecapping both linear and box office revenues as well as residuals spun-out to employees. Disney, as an example, has staked the company’s future on a pivot to streaming and direct-to-consumer sales. In doing so, the company hangs in the unique situation of being formerly run for shareholders & employees to now being run for consumers and employees.

It’s important to understand that Disney underwent the digital shift in pursuit of maximizing shareholder value. Shifting the market’s perception of Disney as a technology business rather than a legacy media franchise would serve to boost earnings multiples and improve returns on capital. It’s likely that the bundled product of Disney+, ESPN+, and Hulu is artificially under-priced to acquire customers and drive top-line growth. Artificially, that is, given that Disney’s direct-to-consumer division has yet to net a profit, despite boasting over 100MM subscribers. This “land-grab” exhibited by the direct-to-consumer segment epitomizes the shift depicted above: Disney is eschewing shareholder interests (free cash flow generation, share repurchases, dividend aristocracy) in favor of more employee and customer-oriented initiatives (top-line growth, consumer surpluses).

Historically, media businesses were known to be shareholder-friendly, passing on price hikes to customers while enjoying ample dividends and free cash flow margins. It didn’t really matter if customers didn’t want to pay for a tertiary channel like ESPN News – Disney’s bundled channels allowed the company to charge more for what was effectively the same amount of content.

Employees didn’t fare too poorly under the old model, either. Top-tier cinematic talent would often get a direct cut of box office sales, yielding seven to eight-figure paydays for high-grossing films. Not to mention, cable’s seemingly endless selection of channels helped to create demand and extend the lifetime value of legacy IP. Airing old movies or TV shows on channels like TBS, ABC, or TNT provided actors and writers with a steady, residual stream of income, while cable customers footed the bill. But, as we discussed prior, Hollywood is confronted by an evolving marketplace. Studios are competing with other mediums of entertainment while content delivery moves from a linear to digital model. Not to mention, the streaming model has yet to demonstrate structural profitability, much to the ire of shareholders. The ongoing writers’ strike makes it apparent that studios will have to increase worker’s compensation, likely working to the detriment of shareholders who have been hoping for profit margins to revert to historical means.

vi) Characteristics of Employee-Focused Businesses:

Employee-ran businesses are typically concentrated in service-oriented industries bolstered by human capital. Technology and IT, as an example, is incredibly human capital-intensive. Software engineers are among the highest compensated employees in the world because their skills & expertise endow their employer with competitive advantages in the marketplace. Because of this dynamic, software engineers and other tech employees are conceivably overcompensated to ensure that they do not depart for a competitor or a fledgling, young startup. The meme of ping pong tables in every tech company’s lobby stems from the industry’s desire to retain talent, even if it means losing some productivity here and there.

Banks & financial services are relatively similar in this regard, these are predominantly relationship-driven services. The value of say, an investment banker, is loosely tethered to who they know and how they leverage that relationship. This became evident in the Silicon Valley Bank dissolution as other banks were quick to try and court SVB’s bankers over to their franchise. Ideally, these bankers would be accompanied by trade secrets and relationships that could eventually translate into underwriting fees, trading commissions, and other banking business.

Perhaps uncoincidentally, financial services, engineering, and technology appear to be among the industries most subject to aggressive non-competes, indicating how valuable their human capital is. These jobs can also be characterized by high degrees of share-based compensation. This, in a sense, serves to “flatten” the Triangle of Capital Allocation by collapsing the shareholder and employee constituency into one body, thus reducing the square footage of their stakeholdership.

“Flattening the triangle”, however, is not a panacea. As we discussed, share-based compensation reduces net income and dilutes existing shareholders. The combination of both might deter outside investors, thus reducing liquidity and hiking the company’s cost of capital.

Equity compensation is not exclusive to public companies, however. Managers of private companies can deliver monetary value to employees in several forms including a tender offer or sale of the business. Notably, SpaceX conducts a bi-annual tender offer for employees, providing liquidity should they wish to capitalize on investor demand. Other companies, particularly in the software space, look to sell their business to a larger platform as a means of boosting distribution and benefiting from a larger resource pool. The acqui-hire trend was particularly salient in the 2010’s as niche software products found easier paths to market under a larger corporate umbrella. Platformification, if you will…

The American automotive industry is perhaps infamous for leaning too heavily into employee-focused capital allocation strategies. General Motors notoriously burdened an $100B pension liability prior to the Global Financial Crisis in 2008 – which was estimated to be $20B underfunded. Indeed, the lack of innovation from legacy automakers like General Motors and Ford is frequently attributed to the company’s pension burdens to which they carry to this day.

vii) Conclusion

“Rule No. 1: Never lose money. Rule No. 2: Never forget rule No. 1.”

— Warren E. Buffett

Businesses are nuanced entities — I accept that it’s not always fair to paint a business as being explicitly “pro-consumer”, or “anti-employee”, or anything of that sort. This is, to a certain extent, why ESG investment funds lack standardization and are often mocked for their resemblance to broad-market indexes. Over the lifespan of an enterprise, a company could find themselves in any of the three corners of the Triangle of Capital Allocation.

The objective of an investor is to figure out how they will get their money back, plus a rate of return. By studying the way in which businesses allocate capital, investors can ascertain the strategies and motivations of company management. Not to mention, understanding the company’s maturity and their capacity to generate shareholder returns. Then again, there is no correct way to run a business.

Accounting “adjustments” can lead to unusual outcomes

So much as the corporate charter will allow such a structure.

Beta (β) is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole (usually the S&P 500).

There are plenty of reasons why a company might be profitable and require financing, but for this example, let’s assume that profitable/cash flowing businesses don’t need additional financing.

Conventional wisdom highlights that public stock prices are representative of the discounted sum of future cash flows, although the Price-to-Earnings ratio (Price per share / Earnings per share) tends to dominate much of the conversation on valuation.

Exxon’s employees presumably also owned a lot of stock!

There are also regulatory considerations, proxy votes, among other hurdles needed to complete an acquisition.