The Great Re-Shoring

Manufacturing comes home, persistent inflation, and protectionism in Latin America

Hey everyone - I really appreciate all of the kind words in response to my last post. While I can’t promise that I’ll post consistently, there’s a lot happening and I need an outlet to articulate my thoughts. I’ll be publishing every so often, and may be lagging specific news events, so apologies in advance if what I write feels dated. Thank you again for allowing me to occupy space in your inbox.

Onto the newsletter!

From the WSJ:

“We’re doing this even though China is way cheaper,” Mr. Madar said. “How good is it to have cheaper components when you cannot get them? For a consumer-products company like us, you need to have super stability in supply.”

The New York-based fragrance seller is among a collection of companies shifting operations back to the U.S. from China and other countries where cheap labor and easy access to factory capacity had far outweighed costs of shipping products across the ocean.

The pandemic and ensuing global supply-chain meltdown have made businesses—from beauty companies and auto manufacturers to global retailers and small businesses—rethink low-cost importing.

One of the earliest themes we discussed in TGC was the decoupling between the United States and People’s Republic of China. While this skirmish was aggravated by Trump-era trade policies, there has always been some semblance of popular support for bringing home domestic manufacturing. Politicians and marketing departments are known to boast “Made in America” labels wherever they can, a subtle nod to American exceptionalism (Or American nationalism, for my international readers) and perhaps a hint of protectionism — but we’ll get back to that in a second.

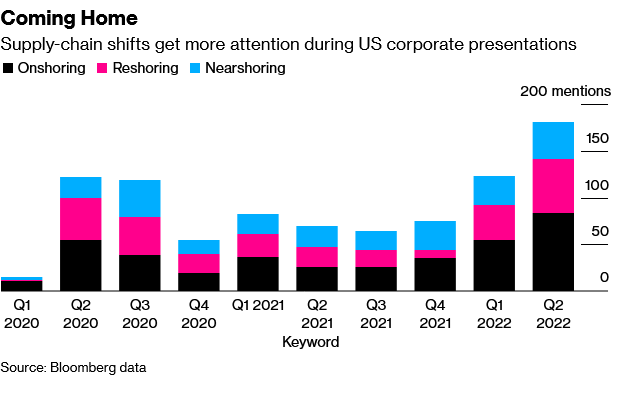

The quote above highlights the fact that the pandemic made it extremely popular for multinational corporations to shake up their supply chain, announcing public-private partnerships with local governments and exuberant capital expenditure projects. Notably in the U.S. — we saw TSMC announce a $16B fabrication plant in Arizona, closely followed by Samsung’s plan to build a $17B fab in Taylor, Texas. Sure, these expenditures could’ve been specifically egged on by the CHIPS Act — which as I write this, hangs in its final deliberations. However, not only is the re-shoring trend active, its reach spans far beyond just semiconductors. More from the article above:

Close to 20% of supply-chain executives surveyed by consulting firm McKinsey & Co. said they had brought some production back to a nearby country in the past year, double the number from a year earlier. More than 30% said they added suppliers in nearby countries in that same period, up from 15% a year earlier. The study included 113 respondents surveyed between March 28 and April 29.

It’s worth highlighting that most re-shoring efforts aren’t undertaken from a noble sense of patriotism, even if we’d like them to be. By contrast, we can assume most companies are economically rational and are thus, profit driven. In the quote above, the manager acknowledges that China would be cheaper, although is not worth the headache for his operation. While I risk extrapolating too much with this anecdote, it does appear that China’s COVID Zero policy is accelerating this trend, prompting companies to explore the market for new suppliers even if it may be more expensive. From a loss minimization framework, the argument reads that companies are anticipating the profits lost from undelivered goods, delayed shipments, or factory closures will be greater than the profits lost from relatively higher input costs, or new supply partners. The discourse is red hot in corporate America, per Bloomberg:

The Russian Invasion of Ukraine is also a material catalyst in this equation — given the looming risk of a Chinese attack on Taiwan. Keep note, the sanctions package saddled on the Russian Federation didn’t technically bar businesses from operating in Russia… Rather, the sanctions have made it so onerous to operate in Russia that there is virtually zero incentive to sustain those business lines. The result has been a little messy, but relatively insignificant in the grand scheme of the global economy. Russia’s economy pales in comparison to China’s, and while the war has sparked a horrific humanitarian crisis on the emerging world, the divestiture of Russian assets has had a near negligible effect on private sector financial statements. Even many of the commodities sensitive to the conflict have returned to pre-war prices.

TGC will always be free for readers. If you would like to support my work, please do so by subscribing and sharing with others.

In contrast to Russia, a sanctions package similarly issued against China in the case of an invasion would have enormous economic ramifications, given the magnitude and reach of China’s economy. The private sector is aware of this: On top of shifting supply chains, American brands and Fortune 500 companies are reportedly being briefed on the peril of war in Taiwan, blueprinting evacuation maneuvers and other emergency measures in case of an invasion. Then again, Russia’s swift expulsion from the global financial system might’ve deterred any immediate plans of invasion. China’s costly response to COVID has brought their economy to a screeching halt — its largest property developers are facing local defaults, other builders are faced with delinquent mortgages, and the birth rate shrank to its lowest on record. While GDP growth has managed to remain in the green, thanks to surging exports, — the latest growth estimates fall far below where the country’s leadership would like them to be.

From the FT:

Where Production is Going (& What it Means for Inflation)

For years, the Chinese manufacturing advantage was obvious: China provided an abundance of cheap labor, favorable regulatory conditions, and proximity to what would eventually become the world’s second largest economy. When analyzing the dis-inflationary forces of the late 20th/early 21st century, one cannot omit China’s enormous labor supply and the innovative boom in Southeast Asia as key contributors.

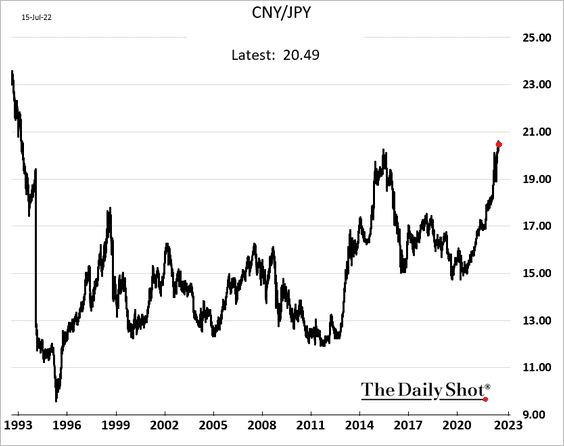

Then again, the China of 20 years ago is no longer. While not technically a developed nation per MSCI and other ratings agencies, it’s clear that China’s demography has evolved to resemble that of a “developed economy” — supported by rising consumption, a burgeoning middle class and consequently, rising wages. Rising wages are inherently good, but become regressive when confronted with a shrinking labor force stemming from an aging population. All things considered, the Chinese market simply does not offer the competitive advantages it once did, given the risks and costs involved. The currency markets appear to be reflecting this new reality — the strength of the renminbi versus competing currencies like the Yen and Won have highlighted the emerging advantage of neighboring exports.

From the Daily Shot below:

From Koyfin:

The dynamics depicted above may lead some to believe our supply chain solutions are obvious: Vietnam can take our manufacturing! The country has already begun to establish itself as a manufacturing powerhouse in Southeast Asia, with the Prime Minister even visiting the New York Stock Exchange earlier this year. Taiwan & Korea continue to maintain a cost and quality advantage in fabricating microchips relative to the U.S. and E.U.. Chile, Bolivia, and Peru will refine precious metals — as they are home to some of the world’s largest copper, lithium, and rare earths reserves, a vital input in the push for green energy and electrification.

Access to these markets is not guaranteed, nor is there any accompanying promise that these markets will provide the same deflationary kickers captured from the Chinese market. While the cost of a shipping container has retreated from earlier this year, the U.S. still suffers from a severe container shortage, aggravating existing supply chain congestion and likely driving up the cost of shipping and storage. Sustained reliance on Southeast Asian manufacturing makes it very plausible that the U.S. supply hiccups in the Pacific could worsen. Vietnam has taken a similarly aggressive stance to COVID, albeit unrelated to China’s policy. In addition — Taiwan, Korea, and Japan, to name a few, all face demography crises similar to China’s. The role of aging societies should really not be understated when discussing inflation: A shrinking labor force reflects rising consumption patterns without the productive supply substitute from younger generations, often leading to structurally persistent inflation.

Populism & Protectionism in South America

On the other hand, South America’s relatively younger demographics offer a promising supply of labor but sit at growing risks of protectionism. Peru, Bolivia, Chile, Colombia, and Brazil — have seen, or will see elections underscored by populist rhetoric, featuring aggressive, government-sponsored economic policies to combat wealth inequality and rampaging inflation. Some candidates — such as Gustavo Petro of Colombia — have proposed initiatives to ban new leases for oil and gas businesses, an industry that comprises nearly 1/4th of the country’s GDP. Other candidates, such as former President Lula de Silva of Brazil and incumbent President Lopez Obrador of Mexico, have highlighted nationalization as a tool to boost domestic economic activity and combat inflation. Finally, the Republic of Chile — once a bastion of neoliberal economic policy — is seeking to overhaul their constitution to repair decades of wealth inequality. Critics of this new constitution warn of rising commodity prices thanks to narrow access to Chile’s copper market, estimated to contribute greater than 25% of global production. While the push for these goals is surely earnest in intention, it’s evident that there will be significant economic and monetary ramifications.

Trivia: Peruvian President Pedro Castillo is known for what prominent article of clothing?

Some leaders, such as Pedro Castillo of Peru, ran on economically illiberal platforms but have begun to back off on their agenda in recent months. Castillo renounced his membership in the Marxist Free Peru party as an explicit commitment to more centrist economic policy. Furthermore, Brazilian incumbent Jair Bolsanaro — who once threatened to leave Mercosur (the South American Free Trade bloc) — has overseen the brokering of multiple bilateral trade deals and has vouched for reducing tariffs as a means of tackling rising prices. Keep note, these reductions only last until 2023 — foretelling a brief reprieve from Brazil’s double-digit inflation, and perhaps an attempt at winning voters prior to October.

The violent ascent of energy prices have made South America home to some of the highest inflation prints in the world — exacerbating existing economic turmoil from the pandemic and causing broader political unrest. Argentina, which we spoke about a few years back, is facing yet another hyper-inflationary episode, with CPI rising over 60% in June. While South America may offer rich natural resources and a healthy labor pool, the risks apparent reveal there is not quite an economic edge to be secured in the continent.

From @CharlieBilello:

The Cost of Re-Shoring

From Bloomberg:

Unfortunately, the tight labor market in cities and states across the US isn’t helping. Despite the economy’s historic post-pandemic comeback, there are still roughly 6 million fewer people employed in the US than before Covid struck. The percentage of unfilled jobs is at its highest level since at least 2001, and the share of Americans in the labor force is near its lowest since the 1970s, according to Labor Department figures.

“There’s just not enough younger workers to replace certain functions, and that’s hit the transit industry very much — especially in the operator position,” Chris Van Eyken, the author of the report, said in an interview.

Ultimately, the last resort for so-called “developed market” production would be the developed markets themselves. As highlighted in the beginning of this post — domestically produced goods and services are extremely popular from a political lens. This philosophy was reinforced in the farewell speech given by outgoing British Prime Minister Boris Johnson — who made sure to share his view that the U.K. was the best place to live and invest. Newly-elected Australian Prime Minister Anthony Albanese won affinity from voters with his ambitions of propelling Australia to green energy dominance, citing the robust mining sector. Furthermore, French incumbent Emmanuel Macron won re-election in the spring on his France 2030 campaign — an effort to position France at the pinnacle of green energy production. At last, the U.S. has embarked on an enterprising push to re-shore key manufacturing processes, with bills supporting semiconductor fabrication and green auto investment at the forefront of the agenda. Quizzically, the aggressive capital expenditure undertaken by these nations and their private sectors sit at contrast to the investment activity seen over the last decade. The U.S. oil patch is a salient example of this — Labor shortages and reduced refinery capacity stem from years of underinvestment following the Global Financial Crisis in 2008 and the subsequent oil bust in the mid-2010’s — resulting in the spiking oil prices we see today.

As we scramble to on-shore additional refinery capacity, we are witnessing the distresses of this operation in real time. Moving the supply chain will take time and will be expensive. Should labor shortages persist in the US, EU, Australia, and elsewhere, we can anticipate sustained inflation for years to come.

Thanks for reading!

Tom

Trivia Answer: Pedro Castillo is known to wear his signature straw hat, also called a chotano.

More reading:

The Great Demographic Reversal — Pradhan & Goodhart

Quality > Quantity

Great work as always brother!