Sovereign Enterprise

Jack Ma's disappearance highlights the current power dynamics found in the relationship between government and business.

Welcome to the Global Capitalist — A free newsletter on international developed, emerging and frontier markets viewed through the lens of history and culture.

Thanks to everyone who offered feedback on the font last week. I think I’m going to keep it this way for the time being.

Rest assured, we do not talk about GameStop, Reddit, or Robinhood today.

Where in the World is (was?) Jack Ma?

For those who may live under a rock: Jack Ma, the wealthiest man in China, had been missing for over two months before resurfacing last week in a video conference. Traditionally, people don’t fret about the day to day activities of CEO’s. Yet, when Ma abandoned his post as a judge on Africa’s Business Heroes, many posited that he in fact, “disappeared” — no doubt a doing of the Chinese Communist Party.

For some time now, Ma and the CCP have been at loggerheads over the country’s stringent banking regulations. Last year at the Shanghai Bund Summit, a Chinese banking conference, Ma was strident with his criticisms of the Basel Accords:

“China doesn’t have a systemic financial risk [problem], China’s finance basically doesn’t have risk, the risk is instead from lacking a system,” said Mr Ma.

“Today banks are still operating with a pawnshop mentality, needing collateral and guarantees are just like pawn shops . . . China’s financial pawnshop mentality is the most serious,” he added.

China’s regulatory crackdown on financial risk in recent years has forced Ant to change its business model several times. The latest challenge to its dominance is the central bank’s rollout of a digital currency which people familiar with the matter say is an attempt by the PBoC to level the playing field between banks and Ant and Tencent.“Supervision and regulation are two different issues,” said Mr Ma. “Supervision is to watch and pay attention to development, while regulation is to manage when there is a problem. Right now we are strong at regulation but lacking in the ability to supervise.”

You can listen to his whole speech here.

Ma’s words ring seasoned with frustration — and rightly so. Recall last autumn in which Ma’s Ant Group, formerly known as Alipay, had been, once again, forced to suspend their initial public offering. Ma had asserted that Ant Group was a technology company, even cosmetically removing “Financial” from their official name last summer. Presumably, a company like Ant Group (a technology company) should receive less regulatory scrutiny than Alipay (a FinTech company) or Ant Financial Group (which sounds like a competitor to China’s state-owned banks).

Over/Under: Can you name the largest bank in China? How many assets do they manage?

However, not long before Ant Group’s highly-anticipated listing, Chinese regulators warned Ma and his executives that their company would receive elevated regulatory oversight, given the novelty of their business. Subsequently, the offering was halted. The Wall Street Journal later would report that Chinese President Xi Jinping personally instructed the shelving of what would’ve been the biggest IPO ever.

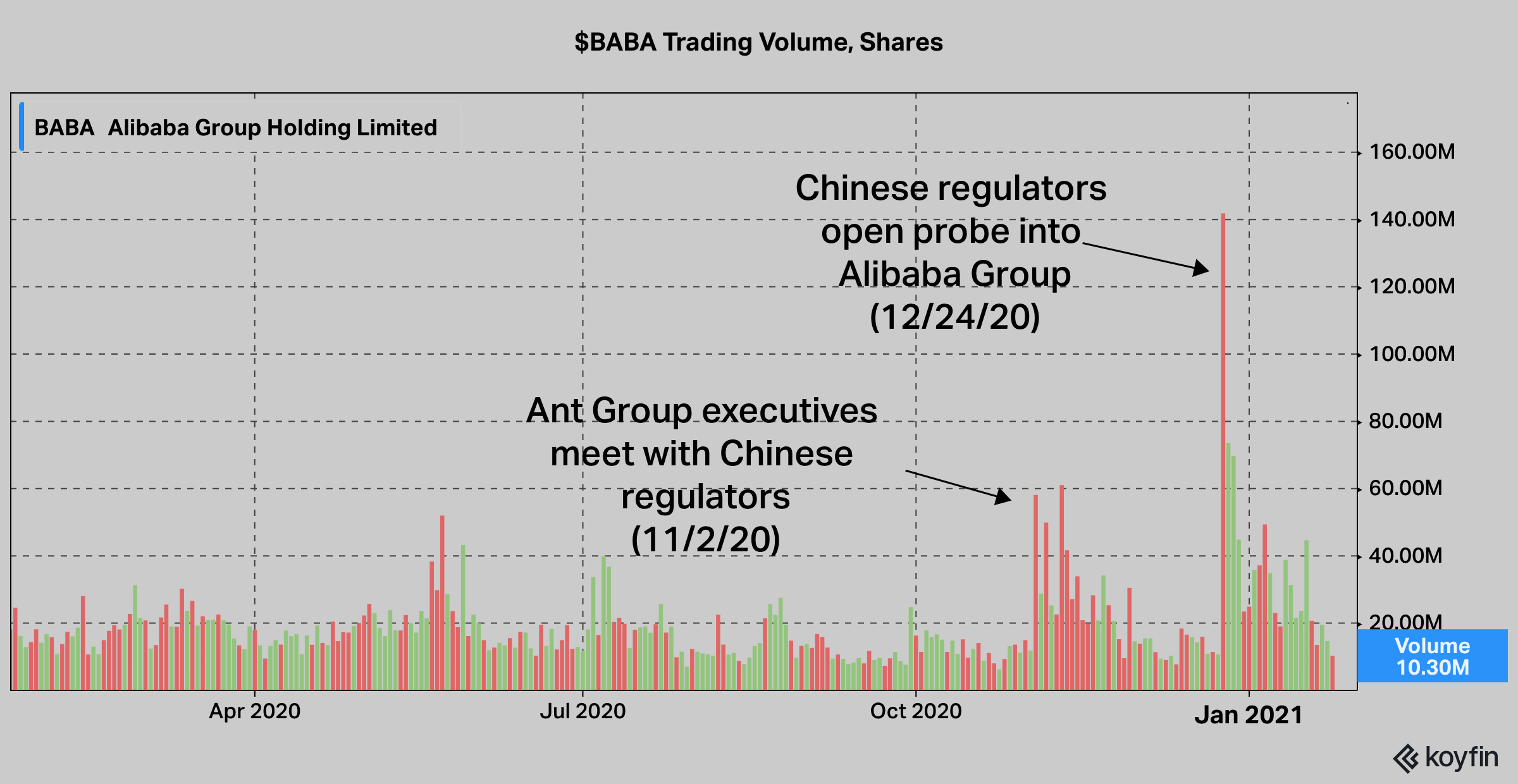

The probe was not limited to Ant. In fact, shares of Ant’s former parent company, Alibaba Group, tumbled on news that Chinese authorities had opened a probe into Alibaba’s business, citing alleged monopolistic practices. Shares of $BABA, which were up as high as 40% on the year, managed to eke out a 5% gain for the full year 2020.

It’s difficult for us here in the States to comprehend the dynamics of China’s rapidly growing market. Chiefly, it is paramount to understand the motivations of the Chinese Communist Party and contingently, Xi Jinping, arguably the most powerful Chinese dictator since Mao Zedong. In the Middle Kingdom, it is glaringly evident that the State carries the ultimate authority. Multi-national corporations can tap into the Chinese market — that is, if their interests align with those of the state. Ma, who had accrued his fortunes as a member of the Chinese Communist Party, had clearly pushed the limits of this boundary.

Alipay is the engine of China’s digital economy. According to the company’s filings, Alipay has over 700 million monthly unique active users, and over a billion annual active users. The company’s edge in consumer data previously endowed Ant with the ability to issue consumer loans at more competitive rates than state-owned lenders. Additionally, the level of liquidity available on the Alipay platform allowed the company’s money market fund, Yu’e Bao (roughly translates to “leftover treasure”) to offer interest rates higher than what competing banks could offer. At its peak, Yu’e Bao was the world’s largest money market fund, managing over $260 billion in assets. In a world dominated by a push to digital, Ant Group stood head and shoulders above their peers.

The ubiquity of Ant Group’s services, however, garnered ire from party officials and regulators alike. Ma’s disappearance, in a way, conveyed Ant’s capitulation to the status quo. In the final blow to Ant Group’s sovereignty, the company announced earlier this week that they would be reorganizing in the form of a financial holding company to be overseen by the People’s Bank of China. Additionally, this new structure will require Ant to maintain cumbersome capital requirements, weighing on profitability.

Now to be fair, there is concerning precedent for this kind of unfettered, unregulated lending. Some of you may recall how the 2015 Chinese Stock Market Bubble could mainly be attributed to the egregious levels of shadow banking and margin lending offered to ordinary investors. The fallout of this crisis throttled global markets as Chinese authorities ordered several high-profile arrests, including a financial journalist and the so-called Warren Buffet of China.

Friendly reminder that this is a free publication. Please consider subscribing below or sharing this post to support my work.

We’re far too familiar with this story... A multinational corporation is forced to reshuffle their corporate governance because they’re vying for a share of the enormous Chinese market. Yum Brands is arguably the most prominent example of this occurrence: On U.S. exchanges, you have the ability to trade $YUM, the restaurant group’s common stock, or $YUMC, a spun-off entity known as Yum China Holdings. They are effectively the same business — they mostly sell the same food and franchise the same brands. However, $YUMC’s business is distinctively Chinese. Their headquarters are located in Shanghai and they’ve independently acquired several other brands in the local Chinese market.

More commonly, a multi-national enterprise will often assemble a “party committee” within the organization to ensure their business is in good standing with those up top. Similar examples can be found in even some of the fastest growing U.S. companies:

In mid-2019 the company had begun an overhaul of its Chinese business, previously part of an operating unit for the Asia-Pacific region. Now, Tesla China would be an independent division reporting directly to the U.S. headquarters. Tom Zhu, a Chinese-born executive who’d been overseeing construction in Shanghai, was put in charge, and he set about making the unit more autonomous and distinct from the rest of Tesla...

Tao made little secret, the employees say, that her priority was to ensure Tesla retained support from the top echelon of the Chinese state. She hung a large organizational chart depicting the upper reaches of the central government and senior officials in key provinces—critical Kremlinology in modern China. According to the employees, she’s said that if she wants to get a message to Xi, she need only go through one intermediary, which would be an astronomical level of access in China. (The Tesla representative denied that Tao has ever made this claim.)

Now, juxtapose the dynamics of business and state in China versus those in the United States, or even Europe for that matter. Not that it is accepted, but businesses commonly circumnavigate policy here in the States. The Silicon Valley ethos, if you will, has seen entire business models manifested on this premise. In the early days of Uber Technologies, the company infamously instructed their drivers to ignore local “For-Hire Driver” laws. Their goal, albeit extremely illegal, championed populist ideals. The company argued that their product was popular so it was policy that needed to adapt.

Similarly, Facebook was born from Mark Zuckerberg’s illicit hacking into Harvard University’s databases. The company would promulgate this culture through Zuckerberg’s infamous instructions to “Move Fast and Break Things”.

Frankly, I don’t find it to be a coincidence that both of these companies are banned in the People’s Republic of China.

Ma, the Meatloaf: China’s second wealthiest man is known by what peculiar nickname?

All of this is basically a long-winded way of detailing the disunity of doing business in China. Enterprises who are jockeying for positioning in China’s market are doing so to capture value from the world’s second largest economy, not for some nefarious, conspiratorial purpose (at least, we can hope...) Executives of publicly traded enterprises have fiduciary obligations to work in the best interest of their shareholders. Shareholders, fundamentally, are interested in high returns on their investment. However, the swelling sphere of party influence in Chinese commerce flashes a warning sign for those adverse to superfluous regulation.

The peril lies in determining what distinguishes a Chinese company from an American company. Apple sells more iPhones in China than they do the U.S. The NBA has more Chinese fans than the U.S. does people. Yes, these companies are headquartered in the U.S., with predominantly American management and employees. At what point, if ever, does this begin to blend?

I believe the most pressing concern with this phenomena is the creeping pressure on Asia’s Tiger Economies. South Korea and Singapore have remained amicable business partners with the Middle Kingdom. Hong Kong’s sovereignty, in contrast, has calved under the pressure from the People’s Republic. Several multinational financial institutions, including the Vanguard Group, have dissolved operations in the city. Dismally, it appears Taiwan is the next target the People’s Republic have sought to recapture.

Speaking of which, I haven’t done a country profile in a while. Next week, we’ll discuss the heightened importance of Taiwan, the Republic of China, in our ever-expanding digital economy.

Trivia

Over/Under: The Industrial and Commercial Bank of China (ICBC) manages nearly $5 trillion in assets as of 9/30/20. The largest American bank by assets, J.P. Morgan, manages about $3.3 trillion.

Ma the Meatloaf: Ma Huateng, or “Pony Ma” is China’s second wealthiest person. Pony Ma’s wealth was created from his stake in Tencent Holdings, one of China’s largest internet media conglomerates.

The Global Capitalist

Follow us on Twitter / Instagram

Follow Tom on Twitter

**If you subscribe through Gmail, please move us from your ‘Promotions’ tab into your ‘Primary’ inbox so you never miss a letter!**

**None of this should be taken as investment advice. Do your own research or speak with an advisor before investing in emerging markets.**