Short Selling a Country

A tweet on New Year's Eve drove me to reexamine our conventional assumptions about what a stock market truly represents.

Welcome to the Global Capitalist — A free newsletter on international developed, emerging and frontier markets viewed through the lens of history and culture.

I got a little carried away in my writing this week but I hope you all will still enjoy.

Happy new year!

— Tom

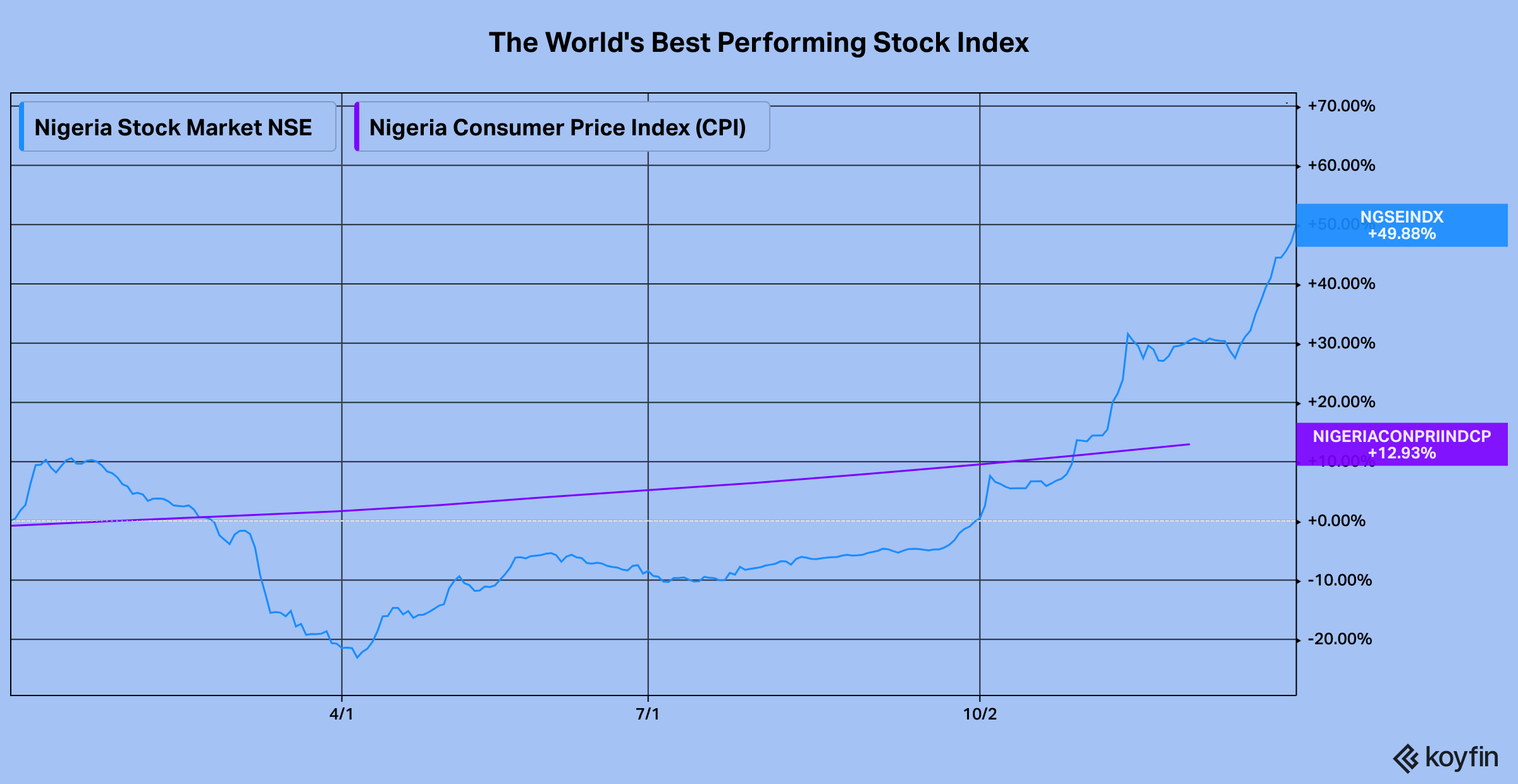

Like I mentioned last week, if you wagered that Nigeria would be home to the world’s best performing stock index, please come to the front to collect your prize.

It’s hard to believe that any stock market would yield a positive return in a year stymied by pandemic, rising geopolitical tensions and economic turmoil. Yet, the Nigerian Stock Exchange All Share Index, against all odds, grew nearly 50% in 2020, outpacing both the Nasdaq Composite and the SZSE Component as the highest-flying stock market across the globe. Mind you — this is not your run-of-the-mill inflationary alpha — which has historically belittled the impressive (nominal) returns of indices such as Argentina’s Merval last year or Venezuela’s IBVC in 2019. Rather, the NSE’s soaring returns occurred in spite the country’s burgeoning risk of becoming a failed state.

For those unfamiliar — Venezuela’s IBVC grew over 5,500% in 2019, a return seldom found in any asset class, with the exception of maybe Bitcoin, or Tesla derivatives. This astonishing figure, however, seems unreal for a reason: It is — and I’ll get to that in a second.

We’ve spoken about Venezuela’s crumbling foundation previously: The country faces an ongoing human rights crisis alongside cumbersome trade embargoes. In tandem, these conditions have provoked crippling hyperinflation and violent civil unrest. The Bolivar was, and is to this day, effectively worthless.

In 2017, the IBVC fell over 30,000 points, or 95%, as incumbent President Maduro’s seizure of the 2018 Venezuelan election capsized the nation’s future economic prospects. Venezuelan equities became a de facto “safe haven” as investors plunged their savings into stocks to hedge against the evaporating Bolivar. In fact, markets boomed so quickly to the point where regulators had to step in and deliberately reduce the market’s valuation to ensure that trading could function properly. Like they say, volatility works both ways.

Fundamentally, however, this ludicrous price action floats the question as to whether stocks prices are derived from marginal demand, opposed to the conventional discovery of intrinsic value.

Cyberpunk 2018: Venezuela released their own cryptocurrency in 2018, what was the name of it? What is it backed by?

Answer at the bottom.

Argentina — in a similar light, is expecting GDP to contract 12% in 2020, delivering the worst economic conditions since the 1998-2002 Argentine Depression. This isn’t a new development, however. Argentina’s economy is currently in its third straight year of recession (which I guess would make it a depression?), attributed to years of capital flight and a lingering debt crisis. The disorder present within Argentina’s economy would only be exacerbated under the one of the most (if not the most) stringent lockdown in the world. Objectively, these restrictions have been a failure, as the country tallies the 12th most coronavirus deaths in the world and the third most in South America. Despite over 200 days of draconian lockdown and curfew, Argentina recently decided to extend lockdown until January 8th. Given the tradeoff between saving their economy or saving their people, Argentina failed to do both.

Efforts from Argentine legislators have been futile in trying to prevent the country’s economic deterioration. In late 2019, outgoing President Mauricio Macri instituted strict foreign exchange controls with the hopes of harnessing the country’s diminishing foreign reserves. In a similar effort last year, the Argentine government threatened onerous taxes on businesses and individuals who use U.S. dollars to service foreign debt obligations. Just last week, the government suspended corn exports to dampen the price of food, which has swelled over 40% YoY. This decision almost immediately spurred a three day strike led by corn farmers, jeopardizing the country’s food supply amidst the lockdowns. Arbitrary price freezes on consumer goods such as televisions and phones have done little else to help compress prices, as Argentine inflation is expected to hurdle 40% in 2020. There is unfortunately little to no reason to believe Argentina will improve anytime soon.

Then again, fundamentals be damned! — The Merval Index blossomed 23% in 2020, mainly buoyed by the country’s robust materials sector. Shares of Ternium SA, the country’s largest publicly traded steel maker, grew 39%, despite a 22% annual reduction in sales through the first three quarters of 2020. Furthermore, shares of Aluar Aluminio, the country’s largest aluminum company, added 50% as quarterly earnings fell to their lowest levels since 2016. Note that Aluar derives 73% of their sales from foreign countries and ships 70% of their product to the U.S. and Mexico.

Curiously, in the Merval’s own version of When a Stranger Calls (“the call is coming from inside the house!”) — shares of the Merval’s parent company ($VALO) helped contribute to the index’s potent performance, seeing shares more than double on the year. Furthermore, BYMA (Bolsa y Mercados Argentina), another Argentine stock exchange, has seen their own shares grow 96% in 2020 thanks to an 117% increase in exchange revenues.

I won’t delve too much into the peculiar principal-agent dilemma of an exchange listing their own shares. I’d recommend giving Ven Iyer’s Malt Liquidity series a read if you’re interested in that topic.

Friendly reminder that this is a free subscription. Please consider subscribing below if you’d like to support my work:

To be fair — all of this is just a long-winded way of stating the obvious: High-performing stock markets don’t always reflect a healthy economy. Heck, they barely reflect a healthy country! Congresswoman Alexandria Ocasio Cortez pejoratively conveyed this sentiment in a controversial tweet on New Year’s Eve:

The worst part is, her joke isn’t entirely inaccurate.

Stock markets are nuanced (and certainly flawed) measures of a company’s health — much less of an entire economy! Stock indices, by extension, are an even poorer reflection of the underlying fundamentals of an economy — especially when considering the variety in benchmark weighting, composition, and trading. Additionally, most major stock indices, if not all, are chiefly dominated by multinational corporations, enjoying a well-diversified portfolio of tangible and intangible assets across the globe. The ubiquity of a multinational corporation’s customers and assets fortifies the substance behind a company’s intrinsic value. That could, by default, transcend the utility of fiat currency. In other words:

If we are to believe that a fiat currency is secured by the full faith and credit of a sponsoring government, and the full faith and credit of said sponsoring government is capitulating, would that make stocks safe haven assets? Asking for a friend.

(Also not investment advice)

Oddly Specific: Can you name the fifth best performing stock index in 2020?

Answer at the bottom.

Just so we’re all on the same page here, stocks prices should go up if:

There is an expectation that free cash flows, discounted at the cost of capital, will increase in the future. (No, seriously.)

The current market value is less than the price that which the marginal buyer is willing to pay.

Citizens of a currency-issuing government flee to non-government assets as a hedge on political chaos. (Anyone look at the U.S. equity markets on Wednesday?)

In that sense, I think Nigeria is a great example of this phenomenon:

Nigeria’s All Share Index, as we mentioned earlier, checked in as the world’s best performing stock index in 2020. Nigeria, as we also mentioned earlier, is barreling towards becoming a failed state. For starters, our Instagram-savvy readers may recall the #EndSARS movement that took place during the fall. Thousands of Nigerian citizens justifiably poured out into the streets to protest against the rogue police unit (Special anti-Robbery Squad) that was known to extort, bribe, and even murder innocent civilians. The movement, which spread like wildfire across Western social media, directed the world’s spotlight on the faltering integrity of Nigeria’s government. Boko Haram, the terrorist group said to have been eradicated under President Buhari, recently claimed responsibility for the kidnapping of 300 schoolchildren in Katsina State. Given Buhari’s history of corruption, there is reason to suspect these kidnappers received ransom for the release of the children. Meanwhile, Nigerian policymakers have blamed their inability to fend off insurgents on a probe issued by the Hague accusing the country’s security forces of war crimes.

The ICC is acting like “another ‘fighting force’ against Nigeria, constantly harassing our security forces and threatening them with investigation and possible prosecution,” Information Minister Lai Mohammed said in a statement emailed Jan. 4. Bensouda’s actions are an “unbridled attempt to demoralize our security men and women as they confront the onslaught from bandits and terrorists,” he said. — BBG

Economically speaking: Nigeria isn’t doing much better. Gross domestic product has shrunk over 21% between 2014 and 2019 and is expected to fall an additional 3.5% in 2020. The World Bank projects that Nigerian incomes will drop to levels not seen since the 1980’s, stemming from the widespread ripple effects of the coronavirus. An estimated 50% of the population is either under, or unemployed, and the job market is failing to accommodate the nation’s boisterous population growth. Currently, the country has more extremely impoverished people (technically defined as making <$1.90 per day) than any other country on earth. By 2022, the World Bank estimates 100 million Nigerians will live in poverty.

Anyone still bullish on Nigerian equities? Bueller?

It’s peculiar — only eleven companies included in NSE30, the sub-index comprised of the country’s thirty largest stocks, yielded positive returns on the year. Of the names that grew, only two companies (Lafarge Africa & Okumu Oil Palm Company) beat the return of the broad market index. Meanwhile, the broad index was littered with moonshot small and micro cap names such as Livestock Feeds Plc ($12M market cap; +225%), FTN Cocao Processors ($4m market cap; +200%), and Neimeth International Pharmaceuticals ($4b market cap; +259%).

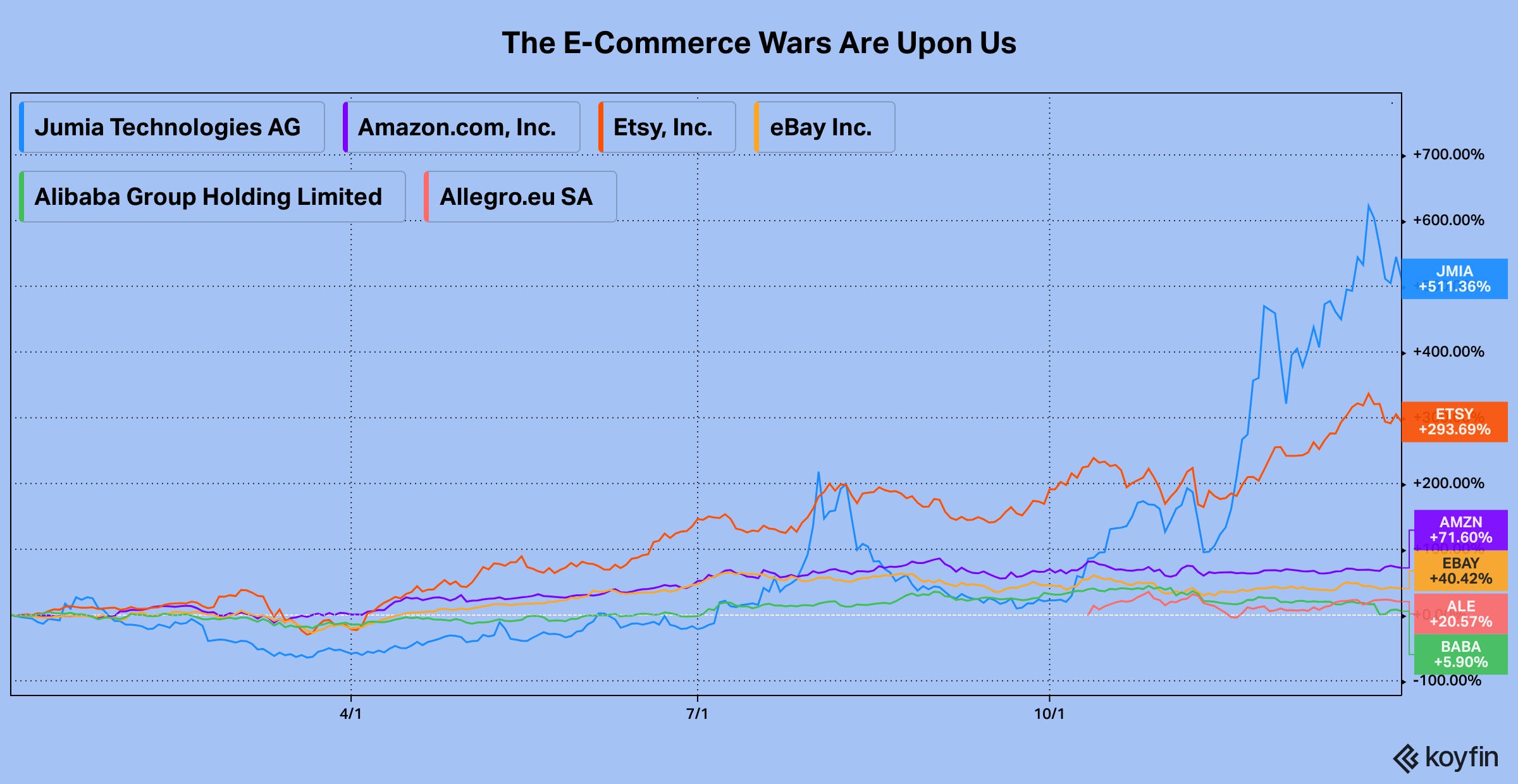

Curiously, Jumia Technologies, a fan favorite amongst retail trading forums, does not trade on the Nigerian exchange, despite being the country’s most popular online retailer. Nevertheless, the success of Jumia’s business indicates that there are abundant opportunities in Nigeria, despite its chaos.

Side note: Each day I grow increasingly puzzled over the viability of e-commerce companies, particularly as they weave in and out of the geopolitical landscape surrounding them. That, however, will be a topic for next week.

Trivia

Cyberpunk 2018: In 2018, President Maduro issued a digital currency called “Petro”. Petro is allegedly pegged to Argentina’s oil and mineral reserves, yet there is no system or formula that demonstrates this peg.

Oddly Specific: Turkey’s Borsa Istanbul 100 (BIST100) grew over 27% last year, checking in as the world’s fifth best performing stock index.

The Global Capitalist

Follow us on Twitter / Instagram

Follow Tom on Twitter

**If you subscribe through Gmail, please move us from your ‘Promotions’ tab into your ‘Primary’ inbox so you never miss a letter!**

**None of this should be perceived as investment advice. Do your own research or speak with an advisor before investing in emerging markets.**