DXY vs. the World

Foreign exchange, economic sanctions, and a looming crisis in EM debt

Hey everyone - Long time, no talk. Apologies for the radio silence, but a lot has happened since last Summer. We’ll get to all of that eventually. Onto the newsletter:

Koyfin Markets

The U.S. dollar reached a new 20-year high on Monday as risk-off sentiment stemming in part from concerns over the Federal Reserve’s ability to combat high inflation boosted the greenback’s safe-haven appeal.

The dollar has risen for five straight weeks as U.S. Treasury yields have climbed on expectations the Fed will be aggressive in attempting to tamp down inflation.

The fortitude of the U.S. Dollar has been a salient, yet curious, theme since the onset of the pandemic. As of this writing, the Dollar Index (DXY) index sits above 100, or roughly around 2017/2020 highs. Of course, the global inflation boogeyman has ensured that all tangential economic discussions be shelved until central bankers and politicians are shamed for decades-high CPI prints and spiking commodity prices. Putting the headlines aside, I'm intrigued by the ramifications of a strengthening dollar in an increasingly fractured global financial system.

In some circles of economic thought - the concept of a strengthening dollar and record-high inflation sit at odds with one another. Fundamentally, inflation implies the erosion of purchasing power, while a stronger currency equates to rising purchasing power over imports and commodities. Foreign exchange and international trade is obviously much more nuanced than that! Crude Oil is selling for nearly $120/bbl - likely exacerbating global inflation, while the DXY remains near highs.

How can this all make sense?

TGC will always be free for readers. If you would like to support my work, please do so by subscribing and sharing with others.

Narrowing Deficit (For Now)

Buoying the country’s fiscal outlook in the near term, the U.S. is expected to rake in a substantial amount of cash from taxes this year and see a dip over the next two years in federal debt held by the public. Both of those boons are expected to be short-lived, however.

After dipping to 96 percent of GDP next year, federal debt held by the public is projected to reach 110 percent of GDP a decade from now, higher than it has ever been. Federal debt will then grow to 185 percent of GDP in 2052, the budget office predicts.

The other week President Biden touted that the U.S. successfully shrank their deficit by over $1 trillion in 2021 with expectations of shrinking the deficit by over $1.5 trillion in 2022. Without giving too much credence to political speak, it’s not clear this windfall was entirely intentional, but it does support the premise of a strengthening dollar. Put simply, higher tax revenue translates into more cash to service debt obligations, easing the burden of debt payments from government bodies. By extension, some economic theories view taxation as a “dollar destruction” process, reducing the supply of currency and subsequently pushing up the “price” of a dollar. If we are to adhere to these theories, the strengthening dollar lines up with record high tax receipts from 2021, derived from increased payrolls, property appraisals, and capital gains bills. Currency appreciation, as we’ll soon learn however, can cut both ways.

The Ruble

A perplexing, albeit fascinating development in the FX market has been the V-shaped recovery found in the Russian Ruble. Immediately following the invasion of Ukraine, NATO countries and their allies swiftly saddled Russia with sanctions, torpedoing the Ruble and blocking the country off from the international financial system. The Russian Federation would retaliate with sanctions of their own, while the Central Bank of Russia would take the policy rate to 20% in order to shore up the Ruble. Russia’s sanctions sought to vacuum-seal capital within the nation’s borders, going so far as to ban dividends and interest payments to “unfriendly countries”. What’s more, Russian commodities would now have to be purchased in Rubles, despite contractual obligations that allowed Dollars and Euros. Yet, despite all of this obstruction, Russia has still not technically defaulted. And while their current account surplus grows wider by the month, the odds of a default are growing daily.

TRIVIA:

Who was the last Asian country to default on their debt? What year did it occur?

Answer below.

In the months since the invasion, the Ruble has not only recovered to pre-invasion levels but has rallied into one of the top performing currencies of the year. Indeed, in a bizarre spasm in foreign exchange markets, the Russian Ruble is, by some measures, the best performing currency in the world. It’s important to note, quotes for RUB pairings have been heavily disputed by local sources. Regardless, the sporadic price action found in their currency tells a unique story about monetary economics and the ongoing economic crisis.

RUB/USD - Koyfin

One could argue that the Ruble’s rally is supported by economic fundamentals: Rising energy prices, a swelling current account surplus, and competitive yields on OFZs are a recipe for strong inflows. In fact, these kinds of factors have been credited for the ascent of other export-heavy currencies such as the Brazilian Real, albeit with a major asterisk. Commodity-exporting countries are actually hindered by strengthening currencies, as they are competing with other commodity exporting nations to offer attractive prices for raw materials.

Given recent events, you can probably see why this is perilous for Russia. Not only is the country confronting the world’s strictest sanctions, but their remaining customers do not share the same demand for oil and gas imports as the EU and the U.S. do. India and China, two of the largest economies yet to issue sanctions against Russia, are both net exporters of petroleum products, and can likely find competitive advantages from a softer currency.

From CNBC:

Following an extraordinary meeting, policymakers opted for another 300 basis point cut, the Bank’s third since an emergency hike of the key rate from 9.5% to 20% in the immediate aftermath of Russia’s invasion of Ukraine, and the imposition of punitive sanctions by Western powers. At the time, the CBR also imposed strict capital control measures in a bid to mitigate the impact of sanctions and prop up the ruble.

“The latest weekly data point to a significant slowdown in the current price growth rates. Inflationary pressure eases on the back of the ruble exchange rate dynamics as well as the noticeable decline in inflation expectations of households and businesses,” the CBR said in a statement Thursday.

“In April annual inflation reached 17.8%, however, based on the estimate as of 20 May, it slowed down to 17.5%, decreasing faster than in the Bank of Russia’s April forecast.”

I find curious in this situation that Russia’s solution to boosting their economy (The World Bank is currently projecting Russia’s economy to contract 10% in 2022) is to cut rates, while the United States plan to tackle a surging greenback and backstop an economic slowdown is to hike rates and draw dollars out of the system.

What does this dynamic imply? The dichotomy is worth examining further.

Real Yields & the Death of the Carry Trade

Readers of this newsletter understand that the U.S. dollar is unique in that it currently stands as the de facto world reserve currency. In this sense, U.S. treasury debt is considered risk-free, given that those securities are not susceptible to credit nor default risk, merely interest-rate risk. The interest on a 10-year treasury, known as the risk-free rate, is also a key input for calculating asset prices and valuations. The risk free rate can also serve as a leading indicator for both U.S. GDP growth and inflation expectations. The ubiquity and significance of this figure is why yield curve inversions often cause such uproar in the financial markets (See April ‘22, August ‘19, December ‘05 of late) and commonly precede recessions.

Furthermore, the significance of these instruments has attracted droves of foreign investors towards U.S. dollar denominated assets as a means of reinforcing their own currency, gaining membership in the “Dollar system”, or simply generating yield. “Chasing yield” in U.S. debt securities had become somewhat of a meme in recent years, a byproduct of dovish U.S. monetary policy responses following the GFC and COVID-19 recession. With perspective, it’s important to note that the ever-memeable Bank of Japan has kept interest rates at or around 0% over the last 20 years or so while the European Central Bank, at least over the last decade, has closely followed suit. The byproduct of zero interest rate policy has proliferated a popular function in FX markets known as the Carry Trade. In this instance, investors could borrow in Yen or Euro denominated securities at low or zero interest rates and deploy capital into yield-bearing U.S. treasuries, collecting a spread in the process. The spiking “cost” of U.S. dollars, however, is threatening the greenback’s role in this process.

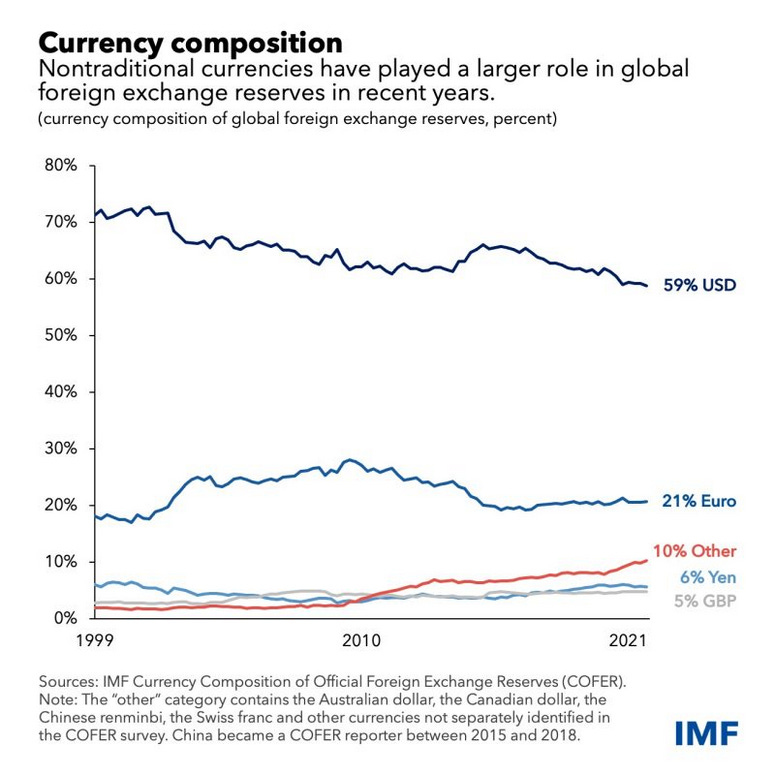

The Yen traded to a 20-year low relative to the U.S. dollar in May, driving up the exchange-adjusted costs of U.S. debt for Japanese investors. The rapid appreciation of the dollar, coupled with the expectation of higher rates in the future, has exacerbated the selloff in U.S. fixed income, stoking further inflation fears. Unfortunately for the U.S., Japan is not the only economy seeing soaring exchange costs. Last month, the Chinese Yuan fell to a 2 year low while the Euro fell to a 5 year low against the dollar. The dollar’s appreciation, coupled with fears of tightening financial conditions amidst an inflationary environment, has led some to speculate that the dollar’s reign as the reserve currency is coming to an end.

There’s a few ways in which people will interpret the above graphic:

Investors are fleeing dollars and dollar-denominated assets because of looming systemic risks, like debasement, hyperinflation, default, etc.

Investors are increasing their exposure to commodity-heavy currencies like Australia and Canada because they can find competitive yields reinforced by raw material exports and reserves

U.S. debt offers noncompetitive yields relative to other countries which has driven foreign investors elsewhere

All of the above could very well be true, although I’m inclined to agree with the latter two bullets. For starters, the emergence of this trend is not inconsistent with the theme of free trade in the late 1990’s (note the beginning of the X-axis). Given this trend, it appears intuitive for countries to diversify their reserves in the face of a globalizing economy. By contrast, I’m less inclined to believe the first bullet because the increase in “Other” currencies can be attributed to the Canadian and Australian dollars’ growing share of reserves. These currencies are virtually dollar system benefactors, given their expansive trade relationships with the U.S. and their allies. You could even lump in the Swiss Franc as a dollar benefactor, given the country’s (unspoken) economic allegiance to the U.S. dollar system.

FRED; 10-yr Breakeven Inflation

Of course, there will always be the risk of Bullet #1. As mentioned above, the U.S. carries one of the world’s largest Debt-to-GDP ratios (albeit smaller than Japan, Italy, and a few others) and relies considerably upon foreign treasury demand (Foreigners hold roughly 33% of publicly held debt, according to Congress) to bankroll trade and the operations of the U.S. government. More saliently, the U.S. is suffering from a bout with inflation, printing some of the highest CPI figures seen in modern U.S. history. Fundamentally, this inflation has provoked a sell-off in fixed income securities, as attractive yields found in a 2% inflationary environment are considerably less appealing in a 7-8% environment.

In a vicious cycle of sorts, the dearth of demand in today’s bond market is exacerbating U.S. inflation expectations and subsequently causing a melt-up in the dollar. If we’re to assume that long duration treasury yields (10 & 30 year maturities) track long-term inflation expectations, one could argue the selloff in those securities occurred in anticipation of persistent inflation. This, in turn, would create enormous demand for dollars that could be redeployed into yield-bearing securities at higher interest rates in the future. This dynamic is consistent with the appreciation in the DXY, while also highlighting the monetary component of anchoring inflation expectations. Inflation, after all, is (at least partially) a monetary phenomenon.

I want to emphasize that creditors still find solace in U.S. debt securities. These instruments are, in essence, backed by the future earnings power of the U.S. economy, the world’s largest economy and consumer market with the most liquid capital markets. Frankly, if treasury auctions are any indicator, there is little reason to believe that U.S. treasuries are losing demand as a safe haven asset.

It is also not entirely certain that Dollar rivals like the Renminbi or the Ruble carry comparable risk/return profiles, especially in light of China’s COVID-zero policy or Russia’s expulsion from the global financial system. In this light, rising yields on U.S. debt will reengage foreign investors alienated by a spiking dollar, anchoring inflation expectations and replenishing liquidity in the treasury markets.

The unfortunate repercussion of this procedure is that higher rates correlate with tighter financial conditions for emerging economies - some of which, have already begun to crack under the weight of a new monetary order.

Who’s Next?

Sri Lankan Rupees; Getty Images/BBC

This extra debt is a worry: during the crisis, poorer countries were helped by ultra-low interest rates in richer economies. That created a flow of cheap money that they could surf. As inflation has taken off in the developed world, however, so interest rates are now rising in response. Investors can no longer risk as much in emerging markets. States cannot afford to borrow.

It is not only higher rates doing the damage. Lower expected growth and new fiscal problems driven by the war in Ukraine are also a worry. The food and fuel price surge is causing havoc. According to the UN, key foods are 19 per cent more expensive than they were in December.

The island nation of Sri Lanka was ravaged by the pandemic, forcing the country into the first default from an Asian-Pacific country since the 1990’s. While Sri Lanka’s tourist-dependent, post-Civil War economy may not serve as an appropriate model for other distressed economies, they are certainly not the only country struggling amidst our new monetary landscape. Argentina, Ecuador, Lebanon are among a litter of nations who fell into default in 2021. This year, the IMF has identified 8 countries they estimate to be in debt distress, in addition to 30 other countries at high risk of default.

As we just examined, the root of this distress appears obvious: Emerging economies can expect to see increasing costs for imports, commodities, and most notably, debt in response to a new monetary regime. As central bankers aim to bridge the gap between monetary and physical constraints, we are once again reminded of the nuances within the capital cycle and the contemporary economy.

Thanks for reading.

Tom (@tgc_tom)

TRIVIA: Pakistan defaulted in 1999, the last default from an Asian country prior to Sri Lanka’s default in 2022.